Thought Waves

Building the Systems of Work Era

We are entering what we describe as the Systems of Work era: a decade in which control of mission‑critical workflows determines durable value creation.

A decade of new company economics

Every structural technology transition produces two simultaneous effects: the repricing of incumbents and the creation of new category leaders.

Markets tend to obsess over the former. Durable wealth is built by participating in the latter.

Artificial intelligence is not a feature cycle. It is a structural reallocation of labour, cost, and competitive advantage across industries. For the first time since the rise of the cloud, software is beginning to execute work rather than merely assist it.

That shift changes everything.

We are entering what we describe as the Systems of Work era: a decade in which control of mission‑critical workflows determines durable value creation.

When software executes work, it no longer simply enhances human productivity. It substitutes for labour input:

- Pricing models change.

- Margin dynamics change.

- Competitive advantage changes.

- Entire categories reorganise around ownership of execution rather than access.

Periods of uncertainty compress multiples and elevate scepticism. They also create asymmetric entry points for disciplined capital.

Fund IV is designed to allocate into this structural transition with an offensive posture: not to defend yesterday's software, but to build tomorrow's incumbents.

.png)

Structural convergence

This opportunity is the result of convergence, not coincidence.

Model capability has crossed practical thresholds. Enterprises are moving beyond pilots and embedding AI into operating budgets. What began as experimentation is becoming restructuring.

Inference costs continue to decline. As execution becomes cheaper, outcome‑based Systems experience expanding margin potential. Structural cost deflation favours those aligned to execution.

Public markets have repriced durability risk. Multiples reflect scepticism toward fragile seat‑based revenue models. Private markets adjust more slowly, creating dispersion between narrative and structural resilience.

Productivity pressure is intensifying globally. Labour costs rise. Efficiency mandates grow louder. Executive teams are being forced to rethink how work is performed.

.png)

Together, these forces create a decade‑long window: to invest in structurally advantaged workflow owners before their dominance is obvious.

The great sorting

The great sorting is the market's durability filter.

Growth unsupported by structural advantage no longer commands premium valuation. Investors increasingly differentiate between revenue velocity and economic alignment.

Software businesses are now evaluated against fundamental questions:

- Is revenue tied to seats or to measurable outcomes?

- Is the product embedded within workflow or adjacent to it?

- Does usage generate proprietary operational context?

- Does governance deepen defensibility?

- Do margins expand as automation improves?

Some incumbents will adapt successfully. Others will plateau. New entrants, unburdened by legacy seat economics, will capture entire workflow categories.

Sorting is not contraction. It is clearance. It removes fragile models and creates space for structurally aligned leaders.

From Systems of Record to Systems of Work

The prior era centred on Systems of Record. These platforms captured, reconciled, and governed information while humans executed the underlying tasks.

The emerging era centres on Systems of Work. These platforms orchestrate and execute tasks across data, models, and enterprise controls. They generate economic outcomes directly.

When labour is executed by software, the economic unit shifts from seat to task to outcome.

- Businesses aligned to outcomes compound as efficiency improves.

- Businesses aligned to headcount compress as labour declines.

This asymmetry defines the opportunity. The most valuable companies of this decade will own execution layers in high‑value workflows: pricing against impact rather than access.

Category creation in the agentic decade

Massive companies will emerge where knowledge work is repetitive, economically measurable, and structurally pressured.

We focus on markets where:

- Labour intensity is high relative to output.

- Workflow frequency creates data compounding.

- Governance is economically material.

- ROI can be clearly expressed.

In such markets, AI adoption is not discretionary. It is inevitable.

The new leaders will combine AI‑native execution harnesses, embedded governance infrastructure, and proprietary context accumulation. They will be measured in economic throughput rather than user counts.

In many categories, this execution layer is unowned. That vacuum is the opportunity of the AI decade.

.png)

Adoption as catalyst

AI adoption requires organisational redesign.

Workflows must be reconfigured. Roles evolve. Governance controls embed deeply.

This transformation is not friction to be avoided. It is the mechanism through which durable position is gained.

.png)

Execution harnesses generate operational data. That data enriches contextual understanding. Improved context increases execution quality. Improved execution deepens workflow dependency.

Only Level-1 operational data compounds defensibility.

Enablement and execution reinforce each other. Early transformation complexity gives way to scalable productisation. Over time, services intensity declines and margin leverage expands.

Adoption difficulty strengthens defensibility.

Corridor advantage

The United States anchors talent density, enterprise scale, and liquidity pathways. It remains the deepest market for AI‑driven company creation and exit.

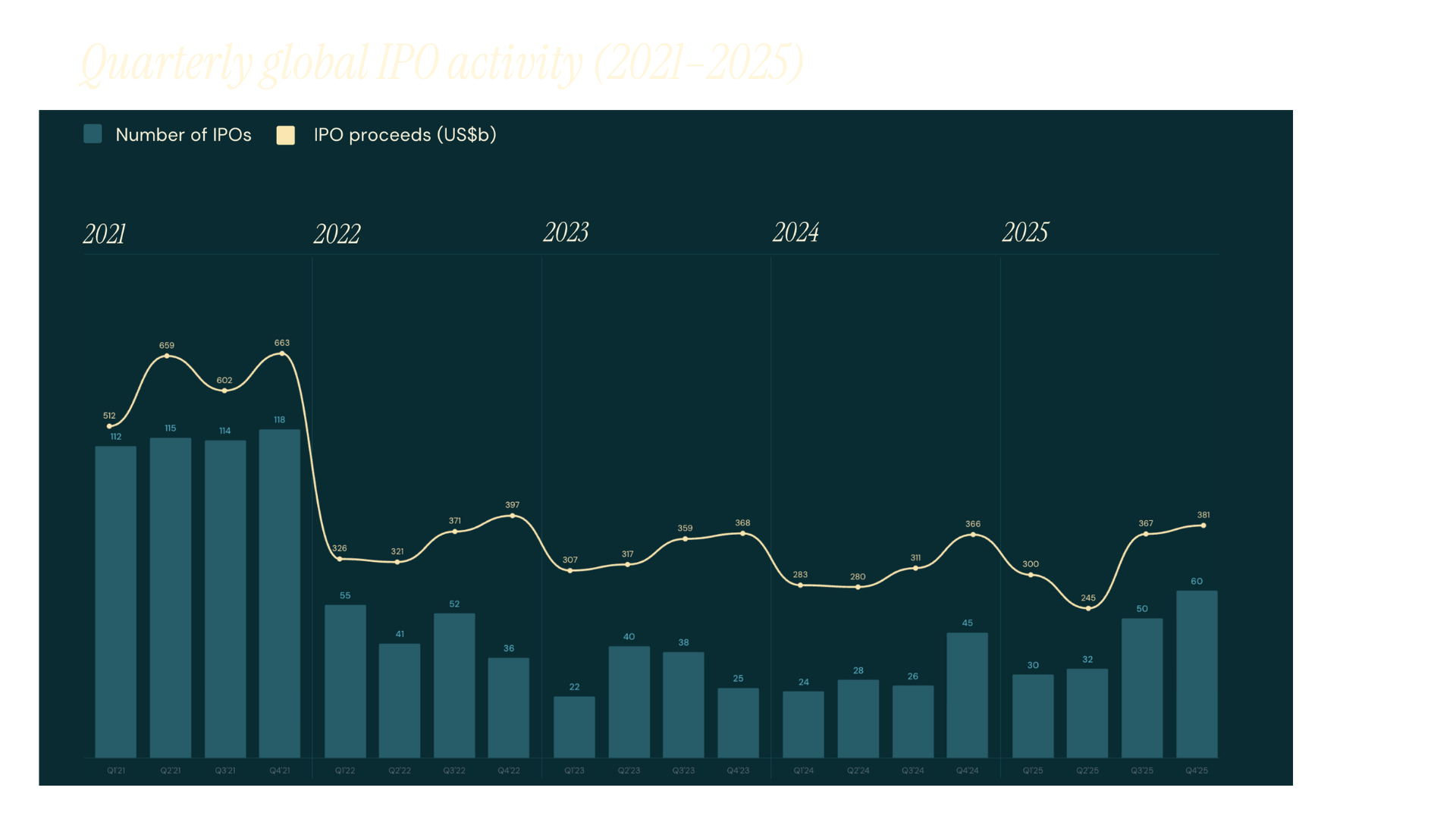

With IPOs largely limited since 2021 and PE still buying, more of the best software assets will be sourced early and stay private for longer.

Australia offers formation efficiency. Productivity pressure sharpens ROI validation. R&D leverage and capital efficiency enable disciplined early build.

Operating across this corridor allows Fund IV to validate efficiently and realise value at scale. This is portfolio physics, not geographic sentiment.

The six signals of durable Systems of Work companies

Early‑stage investing remains founder‑driven. Technical excellence and product depth increasingly determine terminal value. Early ARR velocity often reflects founder capability and market timing.

We seek founders who combine technical fluency with workflow intimacy. They understand economic alignment, not just model capability.

Markets must be structurally inevitable. Adoption pressure must exist independently of hype.

These signals guide how we identify companies structurally aligned with the Systems of Work era. Each reflects a capability that strengthens as automation improves rather than weakens.

- ROI Proof. Clear economic outcomes. The system must deliver measurable economic value inside the workflow. When ROI is provable, pricing shifts from seats to outcomes and throughput, enabling durable pricing power.

- Distribution. Workflow ownership. Durable companies embed directly inside mission-critical workflows. Deep integration creates switching costs and expands distribution through operational dependency.

- Data Defensibility. Compounding operational data. Execution generates proprietary operational data that generic models cannot access.

- AI Operations. Execution speed. The fastest learning Systems win. Companies that run AI across product, engineering, and operations achieve execution velocity that compounds advantage.

- Domain Expertise. Founder-market fit. The strongest founders combine technical fluency with workflow intimacy. They understand both model capability and the economic structure of the industries they are rebuilding.

- Trust Infrastructure. Governance and determinism. Enterprise AI requires auditability, policy control, and deterministic guardrails. Systems that embed governance become trusted infrastructure within regulated workflows.

Our framework guides judgment. It does not replace it. Discipline sharpens intuition rather than constraining it.